During a year when a number of high profile environmental, social and governance (ESG) related events unfolded, sustainable funds[i] assets under management in the US, including mutual funds, exchange-traded funds (ETFs) and exchange-traded notes (ETNs) achieved limited gains. Netinflows, including new fund launches,are estimated at$2.9 billion or an increase of 1.5% relative to 2016.

- While lines in the sector may be blurring in the future, fund flows into the sustainable investing sector should pick up as the segment continues to pivot away from a focus on religious/ethical and exclusionary strategies in favor of integrating ESG factors to improve fundamental investment decisions and with increasing emphasis on shareholder engagement and proxy voting.

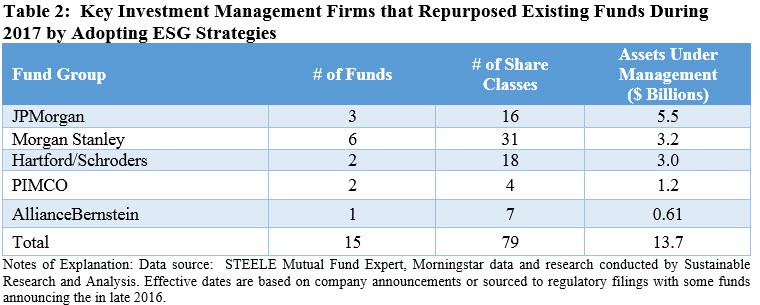

- The trend is expected to accelerate with the entry of traditional investment managers. Firms such as JPMorgan, Morgan Stanley, Hartford/Schroders, PIMCO and AllianceBernstein Investments, have entered the sustainable investment sphere with new and repurposed fund offerings. In the process, these organizations shifted $13.7 billion in assets into the sector with their designated sustainable funds, and two traditional firms moved into the ranks of the top 10based on assets.

- These and other investment managers are expected to continue to introduce more robust product offerings that should lift returns over time. When combined with effective pricing and expanded sustainable oriented disclosures, along with the potential uptake through robo advisor platforms, these developments should serve to attract a larger segment of individual and institutional investors. This shouldalso in time open the market to the $7.5 trillion defined contribution plan retirement market.

- As is, sustainable funds recorded strong absolute total returns in 2017 but large capitalization equity funds, based on the performance of the SUSTAIN Large Cap Index, trailed the S&P 500 Index by 265 basis points. Bond funds and world funds, on the other hand, performed well both on an absolute and relative basis.

- Beyond offering explicitly identified sustainable products, traditional managers stepped up their proxy voting initiatives and engagements on ESG issues with corporations in the US and abroad and this is likely to gain further traction in the coming years. At the same time, engagements with corporations by sustainable fund managers have led to changes in commitments on products, processes or practices.

Sustainable Investing Trends Buttressed by Environmental, Social and Governance Events In 2017

Hardly a day went by in 2017, or so it seems, without coming across some reference on the part of financial commentators and analysts to the growing attraction of sustainable investing and the potential for asset growth in this segment driven by institutional and retail investors seeking to achieve a positive societal outcome while at the same time realizing market based financial results. This was bolstered by third party research and surveys reporting that assets managed in line with responsible investing strategies throughout the globe have surged to almost $23 trillion and about $8.7 trillion in the US on the back of asset growth rates of 33% or even higher since 2014[ii]. Asset owners such as pension funds, insurance companies, sovereign funds, endowments and foundations are leading the transition while individual investors interested in sustainable investing and millennials, in particular, are reported to be 2X more likely than other individual investors to invest in companies or funds that target specific social or environmental outcomes. Buttressing this investing trend were some high profile and not so high profile environmental, social and governance linked events that unfolded in 2017. For example, on the environmental front, extreme weather and natural disasters that were experienced during the year, in the form of violent hurricanes Harvey, Irma and Maria that ravaged Houston,Puerto Rico and other locations, raging wild fires again punishing vast areas of the American West, in particular California, and historically warm atmospheric temperatures. These developments, coupled with the present US Administration’s out of step positioning with respect to climate change, reinforced the sense of urgency associated with the Paris Agreement’s central aim of strengthening the global response to the threat of climate change by keeping a global temperature rise this century to well below 2C°. On the social front, a focus on economic and social inequality continued throughout the year, punctuated, in part, by the rally that turned violent in Charlottesville, Virginia and protests in St. Louis in September. These events were overtaken toward the end of the year, at least temporarily, by sexual harassment revelations and reports of assaults against women in the workplace and elsewhere and rekindling the dialogue around gender diversity and worker treatment practices and, even more broadly, the role of the private sector in addressing these issues in the absence of leadership in Washington DC. As for governance, while lower profile, Wells Fargo was reported to have received regulatory criticism for forcing hundreds of thousands of borrowers to buy unneeded auto insurance when they took out a car loan, for ignoring signs of problems in the auto loan unit as well as its handling of the problems once they were detected. Coming on top of the previous year’s fake credit cards scandal that led to a management shakeup and fines, these developments once again fueled concerns regarding the firm’s corporate governance, ethics as well as worker and customer treatment.

Taken collectively or on a case by case basis, these developments likely influenced the investment decisions of asset owners, individual and institutional investors as well as managers. As the new-year begins, Sustainable Research and Analysis takes a look at last year’s trends and developments in the US sustainable investing sector through the prism of mutual funds and exchange-traded funds that employsustainable investment management strategies and offers its outlook for 2018.

Sustainable Funds Assets Under Management Experienced Limited Gains in 2017 From New Flows, Estimated at $2.9 Billion or an Increase of 1.5%Relative to 2016

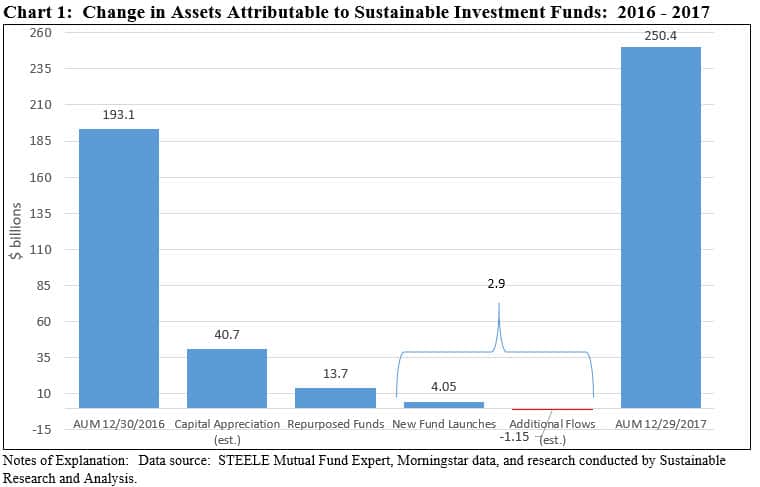

Sustainable funds ended 2017 with $250.4 billion in assets under management (AUM) across 774 funds, including 63 ETFs/ETNs and 711 mutual funds and their corresponding share classes, largely invested in stock, stock-like assets and balanced portfolios. This represents a year-over-year increase of $57.3 billion, or a gain of 30% relative to $193.1 billion in explicitly designated sustainable fund assets at the end of 2016. For perspective, the gain experienced by sustainable funds exceeds by 10% the asset growth posted by the entire mutual funds and ETF industry in 2017. While year-end 2017 data is not yet available, year-over-year figures through November 30, 2017 puts the fund industry’s gain at almost $3.2 trillion or an increase of 19.9%.

While the top line gain achieved by sustainable funds is significant on the surface, a more detailed analysis portrays a different and much less vigorous year-over-year growth profile. In fact, research shows that the asset gains achieved by the sector are largely attributable to capital appreciation and the repurposing of existing mutual funds. These two categories are estimated to have sourced $40.7 billion[iii] and $13.7 billion in assets, respectively, for a combined $54.4 billion or 95% of the year-over-year gain. When combined with assets associated with mutual funds and ETFs/ETNs that commenced operations during 2017, for a total of $4.05 billion, the sector experienced an estimatednet gain of only $2.9 billion or 1.5%. In fact, if not for assets linked to new funds and share classes, the sustainable sector is estimated to have experienced net outflows of $1.15 billion during 2017. Refer to Chart 1. These numbers fall short of expectations given the enthusiastic growth projections made on behalf of sector. A shortage of product offerings with sufficiently long management and performance track records, effective pricing and limited strategy and impact disclosures may be combining to deter investors from investing in sustainable funds in greater numbers. That said, the sustainable investment landscape is undergoing a positive fundamental change as described further along.

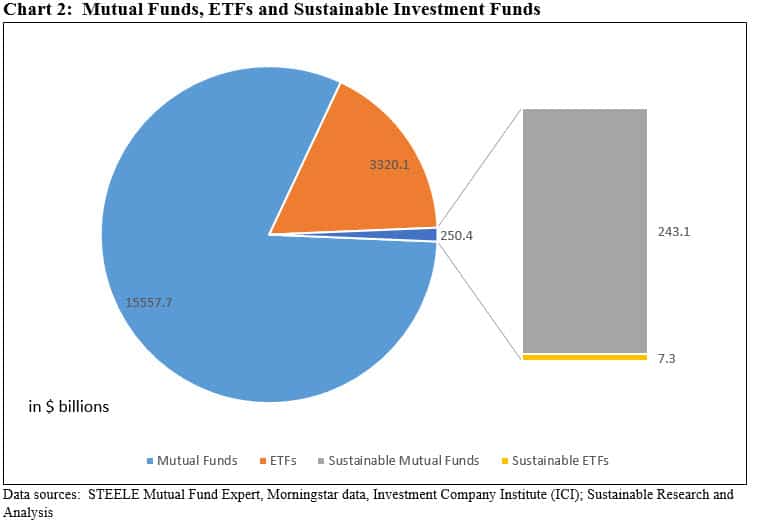

By way of comparison relative to the $19.1 trillion long-term mutual fund and ETF industry as a whole as of November 30, 2017, the sustainable funds segment remains quite small at 1.3% of assets. The broader industry, excluding money market funds, is still heavily dominated by equity and hybrid investments which, at 76% of total net assets versus 97% of the total for sustainable funds and ETFs suggests that in time additional fixed income funds and assets are likely to materialize in this segment. Refer to Chart 2.

Sustainable Funds Sector is Experiencing Notable Shifts: Reduced Concentration in Sector with the Arrival of Traditional Asset Managers Emphasizing ESG Integration Strategies

Fund flows aside, the sector experienced some notable developments and shifts during the course of the year that will likely translate into new funds and improved flows in 2018 and beyond. These developments include:

- The sustainable funds segment expanded with the addition of 24 new fund groups that introduced new products, some as few as one fund, which along with new share classes and additional funds from existing firms, added about $4.05 billion in net assets during 2017. Entering 2017, there were 86 fund groups, offering one or more sustainable mutual funds or ETFs/ETNs. The segment expanded to 110 firms by the end of 2017. There was also merger and acquisition activity in 2017 which led to the merger of assets into the Touchstone Funds uponthe sale of the Sentinel Funds Group that no longer exists and the acquisition of Pax World Management, one of the oldest sustainable asset managers, by UK-based Impax Asset Management Group. Pax will retain the name of its funds.

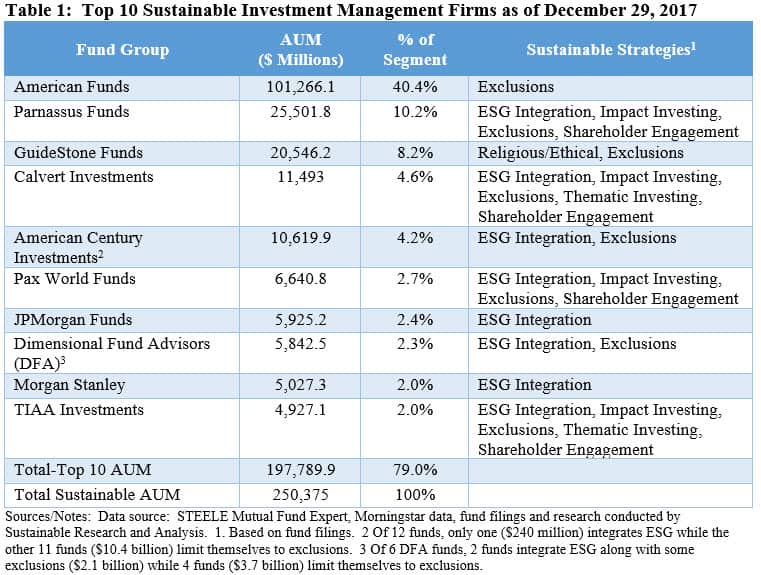

- The segment, which became less concentrated, continued to shift beyond narrower-based exclusionary practices such as avoidance oftobacco and alcohol companies. While the sustainable investments segment remains highly concentrated, with the top 10 fund groups controlling $197.8 billion in assets, or 79% of the segment’s total assets under management, this level of concentration represents a decline from 85% at the end of 2016 due to the entry of new firms and/or expansion of offerings on the part of existing firms. The list of the top 10 sustainable fund groups is still dominated by firms like American Funds, American Century Investments and Dimensional Fund Advisors, or firms that largely employ exclusionary practices, which together account for about 46% of the sustainable segment’s assets under management or an even higher 54% when the religious/ethical oriented GuideStone Funds group is added in. The segment’s sustainable strategies, however, are expanding and shifting beyond narrower-basedstrategies that rely on company exclusions. In contrast, the new firms along with their new investment fund offerings are moving away from a focus on religious and ethical mandates that rely almost entirely on exclusionary practices and instead are embracing more robust sustainable investing strategies such as ESG integration, thematic investing,shareholder engagements and proxy voting.

- Traditional asset managers are entering the space. Just as meaningful for the segment, the transition in favor ESG integration is being led by traditional asset managers. Two new firms, JPMorgan and Morgan Stanley not only launched sustainable products during 2017, but they also repurposed existing funds by adopting ESG strategies that combine with fundamental investment decisions to inform better investment decisions. Refer to Table 1.In the process of doing so, they made their way into the ranks of the top 10 firms in the segment. Also, these two firms are not alone. While they didn’t make their way into the top 10, traditional firms like BlackRock (outside of its iShares ETFs), PIMCO, AllianceBernstein, Fidelity Investments as well as John Hancock have also ventured into the sustainable investing sphere with active and/or passive investment product offerings. In so doing, the competitive landscape is intensifying for firms that have been dedicated to sustainable investing and this makes it even harder for them to compete with their relatively resource-rich counterparts.

112 New Funds and ETFs Add $4.05 Billion in AUM in 2017

Excluding funds that revised their investment mandates by adopting sustainable investing strategies, 112 new funds and share classes augmenting existing funds as well as ETFs were added to the universe of sustainable funds during 2017, with $4.05 billion in assets under management. Highlights include:

Bond Funds

Bond funds in particular recorded gains. Still dominated at the end of 2016 by a cohort of higher/high priced funds and/or funds focused on religious/ethical strategies or thematic approaches and with limited offerings in the investment-grade intermediate term corporate space, the segment consisted of 103 mutual funds/share classes with $15.9 billion in assets and none in the form of ETFs. The sector began to undergo a material shift with the addition of actively managed fixed income products, including thematic funds, from traditional managers as well as ETFs.

- Corporate bond funds. PIMCO Total Return ESG Fund and PIMCO Low Duration ESG Fund changed their names and at the same time modified their investment strategies effective 6 January 2017 to take into account the efficacy of an issuer’s environmental, social and governance (ESG) practices, to exclude securities issued by certain issuers from the portfolio and to engage proactively with issuers to encourage them to improve their ESG practices. In addition to shifting almost $1.2 billion in assets under management into the sector, the funds join previously launched BlackRock and John Hancock funds to expand the offerings that track the Bloomberg Barclays Aggregate U.S. Bond Index. These funds were followed by the repurposing of the JPMorgan Corporate Bond Fund and newly launched corporate bond funds by Brown Advisory and RBC Capital.

- Municipal funds also expanded in number. Two traditional asset managers, JPMorgan and AllianceBernstein, introduced new or repurposed municipal bond funds during the year, bringing the total to 5 management firms and 15 funds/share classes. AllianceBernstein launched the AB Impact Municipal Income Shares, a brand new fund investing in securities that score highly on environmental, social and governance criteria and are deemed by AB to have an environmental or social impact in underserved or low socio-economic communities. The JPMorgan Municipal Income Fund, which has been around since 1993, repurposed itself and became a sustainable fund, based on the fund’s updated February 28, 2017 prospectus. As of that date, this $271.1 fund started to invest the majority of its assets in securities whose proceeds provide positive social or environmental benefits, including investments in green bonds.

- Dedicated green bond funds. While these are not the only two funds, sustainable or otherwise, that invest in green bonds, two dedicated green bond funds, one ETF and one bond fund, were launched during 2017. These include the first green bond ETF, the VanEck Vectors Green Bond ETF managed by Van Eck Associates that commenced operations March 3, 2017. The fund seeks to track the performance of the S&P Green Bond Select Index. The second, an actively managed mutual fund, was launched by Mirova in early 2017. The fund is managed by a unit of Natixis Asset Management, a French Paris-based investment management firm. The funds benefit from an expanding universe of green bonds issued by sovereigns, sub-sovereigns, corporations, financial institutions and special purpose vehicles issuing structured transactions, that in 2017 reached yet another yearly high of $155.4 billion while cumulative issuance stood at about $350 billion.

Equity Funds

78 new equity oriented mutual funds and share classes, the source of $3.3 billion in new assets, commenced operations in 2017. These included launches by existing as well as new managers. New share classes introduced by American Funds’ Washington Mutual for sale through certain registered investment advisor and fee-based programs and the addition of target date funds for institutional investors by GuideStone Funds, both focused on religious/ethical and/or exclusions oriented strategies, accounted for $2.5 billion or 77% of the new assets.

New to the US, investment management firm Arabesque Investment Management Ltd. launched the Arabesque Systematic USA Fund, bringing in a total $18.8 million by year-end. The fund combines Arabesque’s proprietary assessment of non-financial risk factors such as environmental, social and governance issues using a proprietary tool that relies on machine learning and big data, to systematically combine over 200 environmental, social and governance metrics with news signals from over 50,000 sources across 15 languages.

Also, Fidelity Investments introduced two low-cost index mutual funds. One is focused on US equities while the second invests internationally. In both instances, the funds provide MSCI index exposure to companies with high environmental, social, and governance performance relative to their sector peers, as rated by MSCI ESG Research. Excepting for Fidelity’s long-time select environmental and alternative energy fund, these are Fidelity’s first sustainable fund offerings.

Target-Date Sustainable Funds

Mirova also launched a first to market series of target-date ESG funds. Theseries, consisting of 10 funds that employ an asset allocation strategy designed for investors planning to retire within a few years of the target year designated in the fund’s name, follows a sustainable investing approach that selectsU.S. and non-U.S. securities, including emerging markets securities, based on ESG criteria with respect to such issues as fair labor, anti-corruption, human rights, fair business practices and mitigation of environmental impact,seeking a diversified portfolioof investments thatcontribute to a more sustainable future.

While its track record is limited, this is an important product offering that paves the way for making inroads into the defined contribution 401(k) retirement plan market with sustainable investment options. Based on data as of June 30, 2017, $7.5 trillion is held in employer-based defined contribution retirement plans, including $5.1 trillion is held in 401(k) plans. Yet surveys conducted by the US SIF Foundation and Mercer, which specifically focused on sponsors of defined-contribution plans, found that while 14% of the 421 DC plan sponsors responding to the survey offered one or more SRI options, SRI options represented a low percentage of assets of around 1%. Until recently, uncertainty about the compatibility of sustainable investing and a plan sponsor’s fiduciary duty under the Employee Retirement Income Security Act of 1974 (ERISA) was a factor in inhibiting companies from introducing sustainable investing options in 401(k) plans. Guidance in late 2015 issued by the Department of Labor, however, has substantially clarified this issue and made it easier for plan sponsors to offer sustainable investments. An expanding universe of sustainable product offerings with established track records that are effectively priced and which provide impact oriented disclosures would serve to complement the DOL’s action and eliminate barriers to the introduction of sustainable fund investment options in 401(k) plans.

ETFs

The ETF universe of sustainable funds also expanded with the addition of 18 ETFs. In October, Nuveen Fund Advisors, LLC, a unit of Teachers Insurance and Annuity Association of America (TIAA), launched the NuShares ESG U.S. Aggregate Bond ETF, an index tracking exchange-traded fund that seeks to replicate the investment results of the Bloomberg Barclays MSCI US Aggregate ESG Select Index which, in turn, is derived from the Bloomberg Barclays U.S. Aggregate Bond Index. The fund invests in a broad-based portfolio of US investment grade bonds that satisfy certain ESG criteria while at the same time excluding various bonds of companies that are involved in controversial business activities. This is the first broad-based investment grade fixed income ESG oriented ETF within a still small universe of such funds and one for which there is no mutual fund equivalent in the market today.

Attractively priced, the ETF is also the first to seek to replicate the broad investment grade US bond market by covering US government securities, debt securities issued by US corporations, residential and commercial mortgage-backed securities, asset-based securities and US dollar-denominated debt securities issued by non-U.S. governments and corporations (the residential and commercial mortgage-backed securities as well as asset-based securities to be held in the fund are not evaluated and selected on the basis of ESG scores). In doing so, the fund extends coverage beyond the corporate sectors tracked by the two iShares ESG fixed income ETFs launched by BlackRock in June of last year, namely the iShares ESG 1-5 Year USD Corp. Bond ETF and USD Corporate Bond ETF.

15 Funds with About $13.7 Billion Were Repurposed During 2017 by Adopting ESG Strategies

At least five traditional investment management firms repurposed 15 existing mutual funds by adopting ESG investing strategies and adding about $13.7 billion in assets under management to the sustainable sector during the year. In some cases, disclosures around this action are very limited, restricted to simply noting in regulatory filings that in addition to fundamental analysisa company’s exposure to environmental, social and governance factors will be considered. Still, in the case of JPMorgan and Morgan Stanley, the repurposing of existing funds immediately established these firms among the top ten in the sustainable investing sphere, based on assets under management. Table 2summarizes the key investment management firms that repurposed funds during the year:

In addition, several fund companies refined their sustainable strategies during the year. The most notableinclude Dreyfus Third Century, one of the oldest SRI funds, which adopted a broader-based ESG integration strategy. The second is the Alger Responsible Investment Fund that until December 30, 2016 was named the Alger Green Fund but adopted a new mandate that allows the fund to invest in companies identified on the basis of fundamental research as having promising growth potential while demonstrating that they conduct business in a responsible manner relating to ESG matters. Alger expressed the belief that innovative companiesembracing sustainable ESG practices can potentially provide attractive returns for shareholders and support the environment and overall society.

Sustainable Large Capitalization Equity Funds Record Strong 2017 Gains but Lag the S&P 500 while Bond Funds and World Equity Funds Outperform

Bolstered by positive economic data in the US and abroad, steady job growth, rising corporate legislative tax cuts, investors overcame geopolitical uncertainties to drive stocks to new record highs throughout the year. The S&P 500 Index posted a full year total return gain of 21.83% with limited volatility while the Dow Jones Industrial Average closed the year even higher, generating a total return of 25.1% versus last year’s increase of 13.4%. Even such stellar results, however, were eclipsed by the performance of the technology heavy Nasdaq 100, up 32.99%, and emerging markets, measured by the MSCI Emerging Markets Index, which delivered an even greater 37.3% return. Emerging markets posted the best increase since 2009 as well as the highest result across the major assets classes. Investment grade bonds, up 3.54%, turned in the second best performance in the last five years. This exceeded last year’s 2.65% increase and represents the second best performance in the last five years for the Bloomberg Barclay’s U.S. Aggregate Bond Index.

Against this goldilocks backdrop, the universe of 662 sustainable mutual funds and their corresponding share classes, ETFs and ETNs that were in operation for the full 2017 calendar year, regardless of their sustainable investment strategies, recorded an average total return of 20.32%. Returns ranged from eye popping highs posted by share classes of the Morgan Stanley Institutional Asia Opportunity Fund, ranging from 76.82% to 74.85% due to varying expense ratios, to a low of 51 basis points (bps) registered by GuideStone Funds Money Market Investor. Bond funds posted an average return of 4.56% while equity, balanced and equity-like funds ended the year up an average of 23.46%.

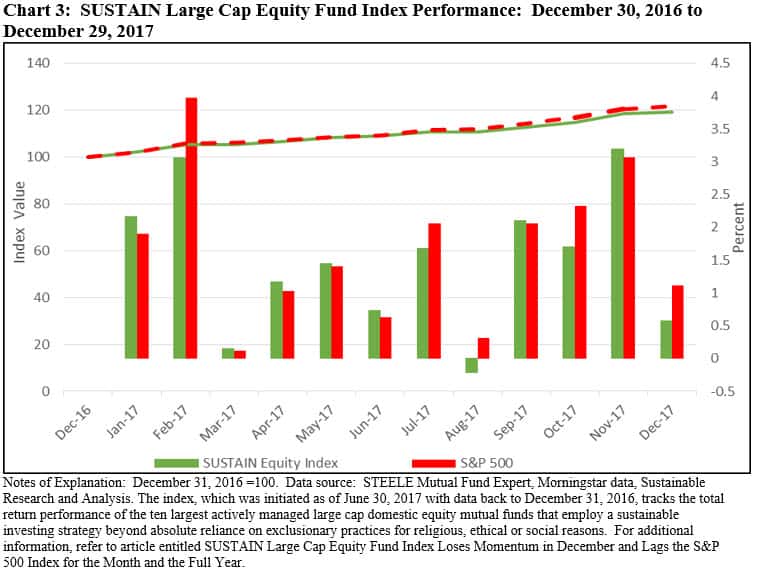

At the same time, similarly managed active mutual funds that employ sustainable investing strategies beyond absolute reliance on exclusionary practices, namely funds emphasizing ESG, performed well in 2017 on an absolute basis and in some cases also on a relative basis. This is illustrated in the results achieved during the calendar year 2017 by the Sustainable (SUSTAIN) Large Cap Equity Fund Index, a fundindex that tracks the total return performance of the ten largest actively managed large-cap US oriented sustainable equity mutual funds. The index delivered strong absolute total return results in 2017 with its gain of 19.18% while the ten funds that comprise the index delivered returns that ranged from a high of 25.79% posted by Calvert Equity A to a low of 15.42% achieved by the Domini Impact Equity Investor share class. For each of the funds that has been in operation over the previous five years, the results achieved last year rank second only to the returns posted in 2013 when the S&P 500 was up 32.39%. That said, the S&P 500 Index, up 21.83% for the year, outperformed the SUSTAIN indexby 265 bps. Refer to Chart 3.

Only one of ten funds that comprise the SUSTAIN Index outperformed the S&P 500 with a gain of 25.79%. The Calvert Equity Fund A overcame its high 1.09% expense ratio and reversed last year’s significant underperformance by its emphasis in 2017 on growth-oriented stocks in the strong performing technology, healthcare and financial services sectors.The fund also benefited from its avoidance of the energy sector which experienced a 2017 decline of about -4.30%. On a 3-year and 5-year basis, however, the fund trailed the S&P 500 Index.

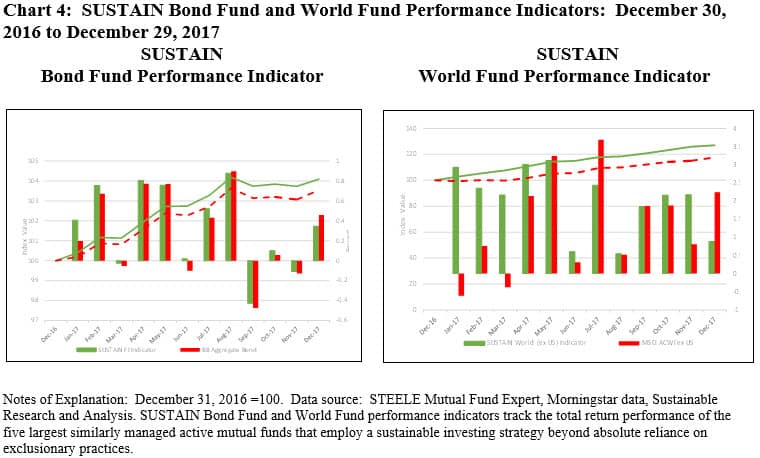

In contrast to the large-cap equity fund returns, smaller cohorts of sustainable bond funds and world funds, ex USA, including developed and developing countries, consisting, in each case, of five actively managed funds with similar investment objectives, produced superior absolute as well as relative results. The Sustainable (SUSTAIN) Bond Fund Indicator and Sustainable (SUSTAIN) World Fund Indicator, each consisting of similarly managed funds that likewise employ sustainable investing strategies beyond absolute reliance on exclusionary practices, were up 4.09% relative to the Bloomberg Barclay’s U.S. Aggregate Bond Index, or an excess return of 55 basis points, and 27.05% relative to the MSCI All Country World Index ex USA (MSCI ACWI ex USA), or an excess return of 940 basis points. Refer to Chart 4.

Stepped Up Reporting and Disclosure on ESG Strategies and Impact Would Accelerate Investor Confidence in Sector

In recent years, investors have been demanding greater disclosure and transparency from corporations about their exposures to environmental, social and governance risks and efforts to address and mitigate these threats. So far there has been limited progress on requiring mandatory disclosures or developing a consensus around voluntary disclosure guidelines in the US or internationally, excepting perhaps for the initiative undertaken by the Financial Stability Board’s (FSB) Task Force on Climate-related Financial Disclosures (TCFD) set up by Bank of England Governor Mark Carney and spearheaded by Michael Bloomberg that on June 29, 2017 published a set of recommendations. The recommendations describe information that both financial and non-financial companies should disclose to help investors, lenders, and insurance underwriters better understand how they oversee and manage climate-related risks and opportunities, as well as the material climate-related risks and opportunities to which they are exposed. While its still early, the Task Force’s recommendations seem to be gaining some traction.

In a similar vein, sustainable investors who seek to achieve a positive societal outcome with their investments need help to better understand how a fund manager’s sustainable strategies are implemented and the range of sustainable outcomes, if any, that are associated with their investments. By providing results that can be tracked, evaluated and compared, investors would be given the opportunity to better understand their fund’s sustainability performance in addition to financial results and, at the same time gain confidence that the strategy is having some positive impact or outcome–optimally in line with investor expectations.

Mutual funds, exchange-traded funds and other similar investment vehicles are required to publish semi-annual and annual reports that describe the financial results achieved by the funds and to compare the results relative to securities market indexes, to disclose securities holdings and to provide other relevant financial information. Some fund firms report to investors even more frequently. Yet when it comes to funds with explicit sustainable mandates, no such requirement regarding non-financial disclosures applies. Some funds limit their disclosures to a short reference to the effect that research analysts seek to assess the risks presented by certain ESG factors. On the other hand, a number of self-described sustainable oriented investment firms do offer regular and, in some cases, extensive voluntary sustainability oriented fund level updates, in particular describing linkages between ESG considerations and stock purchase and sale decisions as well as shareholder engagement activities and results, even as the level and extent of disclosures vary. Some of the larger firms in the sector, such as Calvert, Domini, Neuberger Berman and TIAA, fall into this camp but it’s fair to say that such disclosures are not limited to these firms. It is also evident that such disclosures are evolving and are in the process of improving. For example, Calvert and Neuberger Berman have recently begun to publish fund specific impact reports that describe, through the use of selected metrics and key performance indicators, how portfolios are performing with regard to sustainability and ESG considerations. This is very much in line with what investors should expect to receive from such funds along with expanded insights into the way sustainability considerations are integrated into the investment process. All firms offering sustainable investment products, both actively managed and passive funds, should boost disclosures in this area.

To clarify, disclosures of sustainability ratings or rankings, whether these are applied to individual securities or to funds in the aggregate, much like the Morningstar Sustainability Ratings that were introduced in 2017, are useful in that they offer a point in time opinion about how well the underlying companies held by a fund rank on the basis oftheir ESG factorswhen compared to similar funds. These rankings, however, are not substitutes for outcome oriented disclosures.

Sustainable Investors Attracted to Robo Advisors, but Offerings Are Limited

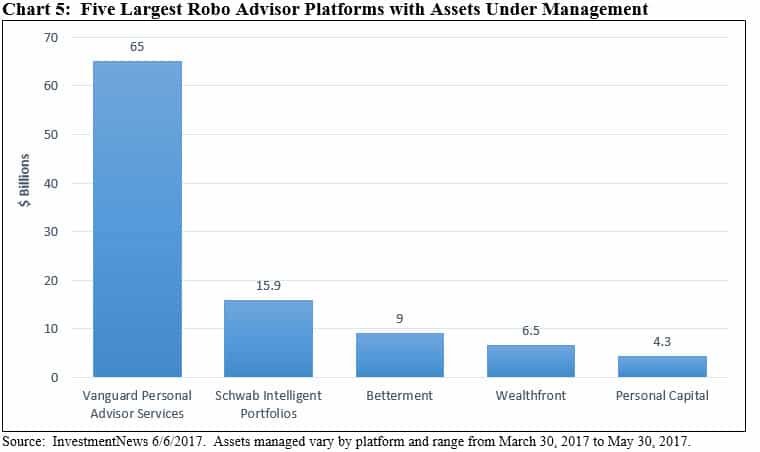

The number of firms offering robo-advisory platforms, online advisors that use computer algorithms to recommend diversified low cost portfolios tailored to the individual clients, continues to expand along with the number of robo advisors offering products that attempt to align portfolios with investors’ values. According to InvestmentNews, the top five U.S. robo-platforms currently have a combined $100 billion in client assets. In addition to Vanguard Personal Advisor Services, the largest platforms in the segment include Schwab Intelligent Portfolios, Betterment, Wealthfront and Personal Capital. According to a 2016 KPMG study, the value of robo advisor controlled assets under management could reach an estimated $2.2 trillion by20120[iv]. Refer to Chart 5.

To attract sustainable investors who express interest in the concept of socially-responsible investments, platforms have either launched with or they have expanded their socially-conscious offerings. TIAA introduced the Personal Portfolio in June of last year with socially responsible fund options thatthat leverage the firm’s expertise in sustainable investing and relies on its own Social Choice funds, the oldest of which commenced operations in 1999. Betterment launched a responsible investing option on its platform over the course of the summer in 2017. The socially responsible investing option also relies on low cost mutual funds and ETFs to integrate environmental, social and governance factors into the investment portfolio based on ESG scores provided by MSCI. At this juncture, however, the SRI portfolio is restricted in that it includes only one SRI fund along with non-SRI funds because Betterment believes that only the U.S. large-capitalization stocks asset class meets the firm’s requirements forlow fees and liquidity.

Earlier in the same year, Motif Investing also launched a values-based investing toolatthe same time, a number of platforms have been established to focus on SRI investing. These include at least the following three firms: OpenInvest, Earthfolio and Grow Invest.

Each of these firms operate with different minimum investment requirement and fee structures and each offers different investment options that largely rely on sustainable ETFs that, with the exception of TIAA,are constructed around indexes that integrate ESG considerations or pursue thematic investing strategies. In each case, sustainable investor profiles supplement financial and risk considerations to fashion a recommended investment portfolio. That said, an investor’s sustainable goals and objectives are very broadly qualified and fund selections do not appear to be subjected to a nuanced evaluation process.

Some of the Largest Traditional Managers Stepped Up Their Engagement and Proxy Voting on ESG Issues

Beyond exercising their stewardship responsibility to vote proxies on behalf of mutual fund and ETF investors at annual shareholder meetings, mutual fund managers can also engage in direct discussions with senior executives and directors of companies in which the funds invest for the purpose of advocating a point of view and/or potentially influencing their behavior. During the past year, in addition to shareholder engagements led and supported by established and more active sustainable investment management firms such as Boston Common, Calvert, Domini, Pax World, TIAA and Walden Asset Management, some of the largest traditional management firms stepped up their engagements on ESG issues and disclosures with corporations in the US and abroad. Such efforts, which are expected to gain more traction, will likely serve to blur the lines between designated sustainable funds and firms that become more active in corporate engagement activities and proxy voting.

BlackRock, the largest asset management firm in the world, was reported to have sent letters from its corporate-governance team in December to about 120 companies, urging them to report climate dangers in line with the recommendations of the Financial Stability Board’s Task Force as those in the energy, transportation and industrial sectors. This was on top of BlackRock’s 2017 annual letter to corporate CEOs written by Laurence D. Fink, CEO, which for the second year in a row, highlighted the firm’s view that companies should devote more attention to issues of long-term sustainability and improve disclosure of their annual strategic frameworks for long-term value creation. This message was kicked up a notch in BlackRock’s just released 2018 letter, that, in the mold of silicon valley H-P pioneers David Packard and William Hewlett, calls upon chief executives to think not only about delivering financial results but to also recognize the responsibility of companies to address broader societal challenges and to show how their companies are making a positive contribution to society.

Vanguard, the second largest asset management firm worldwide, outlined in its 2017 Investment Stewardship Annual Report the firm’s commitment to investment stewardship and discloses that the team devoted to this activity has doubled in size since 2015 to more than 20 analysts, researchers, and operations team members. The report also notesthat for the first time Vanguard’s funds supported a number of climate-related shareholder resolutions opposed by company management. Vanguard is also discussing climate risk with company management and boards more than ever before and is committed to engaging with a range of stakeholders to inform its perspective on these issues, and to share its thinking with the market, its portfolio companies, and investors. At the same time, Vanguard successfully pushed back on a resolution to make an ongoing commitment to genocide-free investing within its funds, and in particular for targeted divestiture from companies that support government-sponsored genocide in Sudan, submitted for consideration at its October 2017 Joint Special Meeting of Shareholders in Scottsdale, Arizona. While acknowledging that the humanitarian issues are of consequence and deep concern, Vanguard argued that meaningful long-term solutions to these issues require diplomatic and political resources to come together to implement change, that the funds are compliant with all applicable US laws on this matter and in addition the proposal would interfere with the advisors’ fiduciary duty to manage funds in line with their investment objectives and strategies. Finally, Vanguard added that the divestment contemplated by the proposal would be an ineffective means to implement the social change it seeks.

The third largest management firm, State Street Global Advisors (SSGA), issued a memo and press releasein March 2017 calling on 3,500 global companies, representing more than $30 trillion in market capitalization, to increase the number of women on corporate boards. In a significant shift, SSGA indicated that it will vote against the chair of a board’s nominating and/or governance committee if a company fails to take action to increase the number of women on its board. SSGA has been following up on this campaign and in November announced that it will expand its effort beyond the U.S., U.K. and Australia to big Japanese and Canadian companies.

Another indication of the changing ESG sentiments on the part of more traditional managers, the three firms, in an apparent reversal, were reported to have lent their support and voted in favor of a proxy proposal submitted by the New York State Common Retirement Fund for consideration at the May 31, 2017 meeting of Exxon Mobil shareholders requesting that starting in 2018 ExxonMobil publish an annual assessment on the company oil and gas reserves and resources under a scenario in which reduction in demand results from carbon restrictions and related rules or commitments adopted by governments consistent with the globally agreed upon 2 degree target. For the first time, investors with 62.3% of shares voted in favor of the resolution.

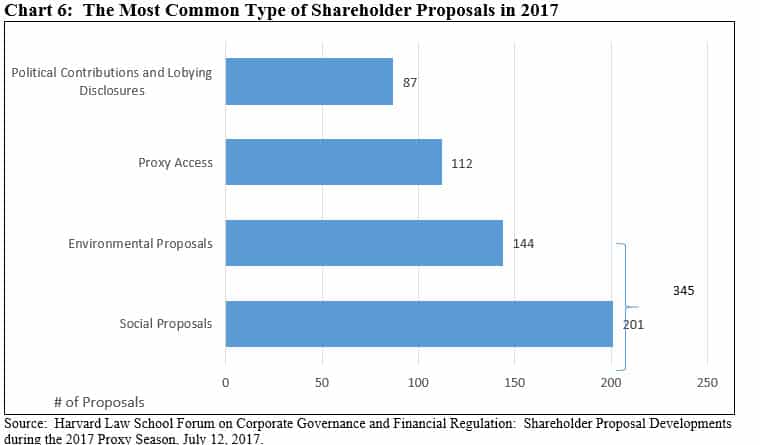

More generally during the 2017 proxy season, there was a renewed focus on key corporate governance principles and a heightened focus on environmental and social issues by institutional investors. Across four broad categories of shareholder proposals, including governance and shareholder rights, environmental and social issues, executive compensation and corporate civic engagement, the most frequently submitted were approximately 345 proposals covering environmental and social topics. Further, there was an unprecedented level of shareholder support for environmental proposals. Refer to Chart 6.

These developments complemented engagement efforts with portfolio companies in an effort to bring about improvements in corporate practices on environmental, social and governance issues in the US and abroad.

For example, according to Boston Common as reported in its 2017 Annual Report, the firm, either in a leadership role or along with other investors, engaged at some level 195 companies that led to 44 significant changes in commitments on products, processes or practices with companies. Some of the impacts reported by Boston Common include:

- Over 23 out of the 28 of the world’s largest banks now have policies to enhance due diligence for carbon intensive sectors and to increase funding for renewable energy.

- PepsiCo adopted new global reformulation goals to reduce salt, sugar, saturated fat and transfat, one of 22 companies to improve management of obesity and/or under-nutrition issues following assessment by the Access to Nutrition Index.

- Google, Microsoft, and Samsung under the Electronic Industry Citizenship Coalition’s new Raw Materials Sourcing Initiative joined 22 other companies to ensure the mining of cobalt does not involve child labor or contravene other environmental and social red lines.

- Mitsubishi UFJ Financial Group, Standard Chartered and PNC Financial adopted better guidance and/or assessment criteria with clients that risk the world’s ability to achieve the Paris Agreement goals.

- Air Liquide, BMW, and National Grid reported steps to improve operational energy efficiency including energy and water use, emissions and waste.

- Leading U.S. pharmacist CVS Health added 100 chemicals of concern to its Restricted Substances List for its CVS brand products. In April 2017, CVS announced its intention to remove all parabens, phthalates and the most prevalent formaldehyde donors across nearly 600 beauty and personal care products by the end of 2019.

[i] Sustainable funds refer to designated mutual funds, exchange-traded funds and exchange traded notes that employ sustainable investing strategies. Sustainable investing is an umbrella term that encapsulates social investing, SRI investing and ESG investing andrefers to the idea that investing in sustainable companies permits investors to achieve long-term competitive financial returns while at the same time attaining a positive societal impact. While it’s been changing somewhat, this concept captures a range of four prominent investment approaches or strategies. These are: (1) Screening out or excluding companies from investment portfolios for a variety of reasons, (2) Impact investing and thematic investing or investing to achieve a targeted social or environmental objective that is measurable, (3) Integrating environmental, social and governance (ESG) considerations as a proactive and integral component of the investment research and portfolio construction processes, and (4) Shareholder and bondholder advocacy and engagement in an effort to influence corporate behavior and proxy voting.

[ii] Global Sustainable Investment Alliance (GSIA) and Forum for Sustainable and Responsible Investment (US SIF).

[iii] Capital appreciation estimated based on returns achieved in 2017 by equity, equity-like and balanced funds as well as bond funds.

[iv] Source: KPMG Robo Advisory Catching Up and Getting Ahead