Stock and bond markets worldwide posted excellent returns in 2019 bolstered by strong December gains: S&P 500 added 3.0% while the Dow Jones Industrial Average and Nasdaq Composite recorded 1.9% and 3.6% increases.

Stock and bond markets worldwide posted excellent returns in 2019. The major US stock indices ended the last day of the year on a positive note, bolstered by encouraging news that the US China Phase 1 trade agreement will be signed on January 15 and signaling a significant de-escalation of trade tensions between the two nations that have affected markets throughout the year both positively and negatively. This factor, combined with interest rate cuts, Fed liquidity, easing anxiety regarding the strength of the US economy and prospects that the longest expansion in US history will continue, moved markets higher in December notwithstanding lingering geopolitical as well as domestic political uncertainties linked to the President’s impeachment proceedings. The S&P 500 posted a total return gain of 3.0%, while the Dow Jones Industrial Average and Nasdaq Composite recorded 1.9% and 3.6% increases. Outside the US, developed and emerging market equities posted even stronger returns, with the MSCI ACWI ex USA (Net) gaining 4.3% and emerging markets climbing 7.5%. Across other asset classes, investment-grade bonds continued to decelerate and dropped -0.1% while gold and energy, in that order, recorded increases of 3.6% and 6.9%. Within the Energy sector, natural gas was the only commodity to fall back, giving up -3.0%.

Against this back-drop, sustainable mutual funds and ETFs across all categories combined posted an average 2.29% total return. More targeted, the Sustainable (SUSTAIN) Large Cap Equity Fund Index gained 2.92% while the SUSTAIN Foreign Equity Fund Index and SUSTAIN Bond Fund Index generated total returns of 3.53% and -0.17%, respectively.

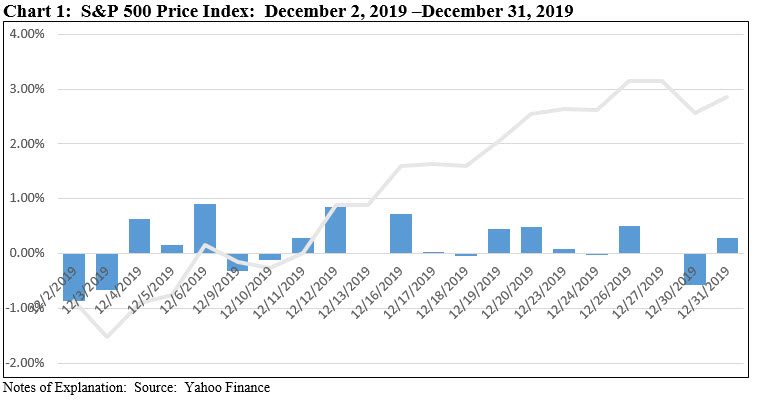

Starting the month of December in the red, the S&P 500 Index hovered in negative territory until December 11 when it kicked up and registered successive but small, less than 1%, gains thereafter. Refer to Chart 1. The market was encouraged by vows on the part of the European Central Bank as well as the US Federal Reserve to support their respective economies. In the US, the Fed’s remarks were made following its decision to keep interest rates on hold. Also during that same week, the Conservative Party led by Boris Johnson won the United Kingdom’s election and in the US the announced US–China Phase 1 mini deal halted the December 15 tariff increases. At the same time, investors were not deterred as the House Judiciary Committee approving two articles of impeachment against President Trump. These developments, reinforced by a string of positive economic news, sustained positive investor sentiment for the remainder of the month of December that led to a series of new market setting records. The Dow Jones Industrial Average and S&P 500 posted new record highs on December 27th and the Nasdaq Composite did so on December 26th. This put the stock market in the US at very high trading levels that, by some measures, such as the Cyclically Adjusted Price Earnings (CAPE) ratio, signaled a note of caution. The ratio now stands at 31, reflecting a level observed only twice before—in 1929 before the stock market crash and in 1999 just before the internet bubble drop. Yet, earnings have stagnated recently and earnings estimates for calendar year 2020, even as they are ascribed an above average earnings growth rate of 9.6% at this time, are likely to ratchet down.

The U.S. economy is entering 2020 along a path that many believe supports the continuation of the longest economic expansion in US history. Real gross domestic product (GDP) increased 2.1% in the third quarter of 2019, according to the “third” estimate released by the Bureau of Economic Analysis in late December. The growth rate was unrevised from the “second” estimate released in November. In the second quarter, real GDP rose 2.0%. Moreover, consumer spending which accounts for almost two-thirds of U.S. economic activity was showing signs of improvement. Per the Commerce Department, consumer outlays increased 0.4% in November, its strongest gain since July. The labor market is tight, the unemployment rate is at a 50-year low and real disposal personal income also increased at a 2.9% annual rate in the third quarter. Unless derailed by geopolitical and domestic political developments, these and other positive indicators suggest that the economy will keep expanding but, based on economic projections, at a slower rate. For example, Morgan Stanley’s base-case outlook calls for U.S. GDP growth of 1.8% in 2020.

The 4th quarter: S&P 500 added 9.1%, DJIA increased by 6.7% and Nasdaq Composite gained 12.5%

Benefiting from successive monthly gains, stocks markets in the US and overseas posted strong growth rates in the fourth quarter. The S&P 500 added 9.1%, the DJIA increased by 6.7% and the Nasdaq Composite charged ahead with a gain of 12.5%. 10 of eleven large-cap sectors also recorded increases, with Information Technology and Healthcare both adding 14.4%. Real Estate, on the other hand, gave up -0.5%. Developed and emerging markets in Europe, Far East, Asia and Latin America also recorded strong gains ranging from a low of 7.1% for the Pacific Region to a high of 14.8% delivered by Eastern Europe, as measured by the MSCI regional international indices. Local markets such as Taiwan, Russia and China posted gains of 18.0%, 17.1% and 14.7%, respectively. The SUSTAIN Indices followed suit, but in each case lagged behind their conventional indices by as little as 18 bps and as much as 66 bps.

The year 2019: S&P roars back with a gain of 31.5%; bonds gain 8.7%

The year in stocks and bonds experienced an unexpected reversal after large cap stocks tumbled some 15% between the end of November and December 24, 2018 on US-China trade uncertainties, recession fears and tightening monetary policy. After ending the year down -4.4%, the S&P came roaring back in 2019 to post a gain of gain of 31.49%, the best gain since 2013 and 25.4% points above the 6.1% average for the last 20 years. The DJIA gained 25.3% and the Nasdaq Composite lead with a gain of 36.7%. Stocks and bonds benefited from falling interest rates, Fed liquidity, receding trade tensions and rosier expectations for economic growth. Growth stocks across the small and mid-cap market spectrums outperformed value stocks while large cap growth and value stocks performed on par. Very large growth stocks (i.e. top 200) outperformed very large value stocks while large caps were just about even. At the same time, small cap stocks fell behind their large cap counterparts by as much as 8.3%, depending on the benchmark.

As for bonds, the Bloomberg Barclays US Aggregate Index added a whopping 8.7% in 2019, the best annual results in the last ten years and 3.7% higher than the 20-year average. Even better 2019 results were posted by long-dated US Treasuries, up 15.1% while US credit added 13.8% as the environment throughout the year remained supportive.

Markets outside the US didn’t reach the highs achieved in the US. The MSCI ACWI, ex USA (Net) was up 21.51%, Europe and emerging market composite came in even lower while a number of national indexes, such as Russia and Taiwan, in particular, gained 52.7% and 37.7%, in that order.

Sustainable (SUSTAIN) Large Cap Equity Fund Index misses S&P 500 by 10 bps

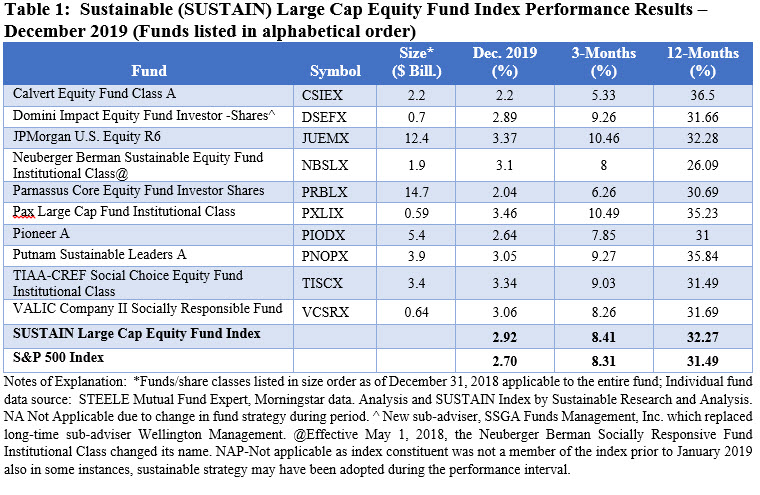

Off by 10 basis points, the SUSTAIN Large Cap Fund Index lagged the S&P 500 for the fourth consecutive month as only four of the ten fund constituents underperformed in December. The Pax Large Cap Fund Institutional Shares led with a 3.46% return, bolstered by the $766.3 million fund’s overweight exposure to the technology sector that gained 4.5% in December as well as stock selection. In particular, above index exposure across its top five holdings, including Apple, Microsoft, Amazon, P&G which was added in the first part of the year and was viewed as an ESG leader, and Merck & Co., all performed well in December. Returns for these five stocks ranged from 2.5% to a high of 9.9% posted by Apple which accounted for 5.62% of the fund’s holdings. At the same time, the fund’s reduction in its energy position to 0.0% ahead of December when energy was up 6.0%, likely detracted from its performance. Two other performance leaders include JPMorgan US Equity R6 and TIAA-CREF Social Choice Equity Fund Institutional Shares that added 3.37% and 3.34% in December. While ranked second in December, the JPMorgan fund was the best performer over the previous two months and has delivered an above benchmark return of 10.46% in the fourth quarter. Refer to Table 1.

At the other end of the range was Parnassus Core Equity Investor. The fund, which seeks low turnover and invests with a high conviction in approximately 40 holdings while avoiding investments in companies engaged in the extraction, exploration, production or refining of fossil fuels, trailed the S&P 500 by 98 bps in December and 281 bps in the last quarter. The fund’s overweighting in industrials while at the same time avoiding the energy sector likely detracted from its performance. Other lagging funds included Calvert Equity A which fell behind with a 2.2% return while still retaining its top performer status for 2019 and Pioneer A that generated a 2.64% return and now also lags behind the S&P 500 for the quarter and 12-month interval.

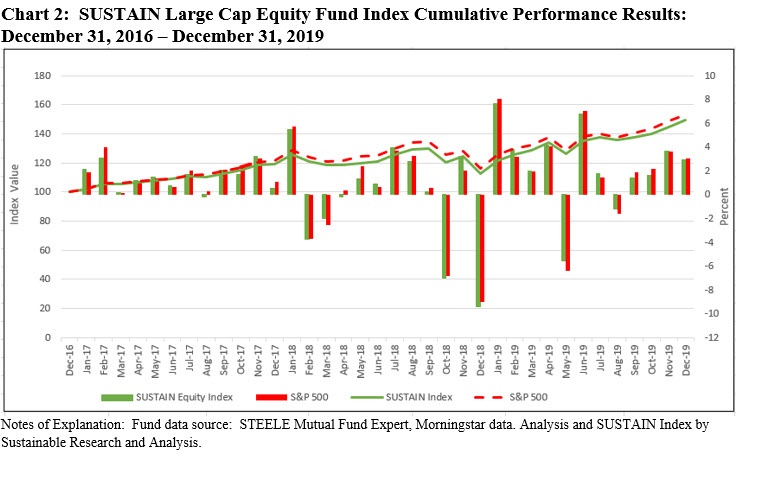

Over 2019, the SUSTAIN Large Cap Equity Fund Index outperformed the S&P 500 but since inception as of December 31, 2016, the Index is up 49.2% versus 53.1% for the S&P 500. Refer to Chart 2.

Sustainable (SUSTAIN) Fixed Income Fund Index lags for the second consecutive month

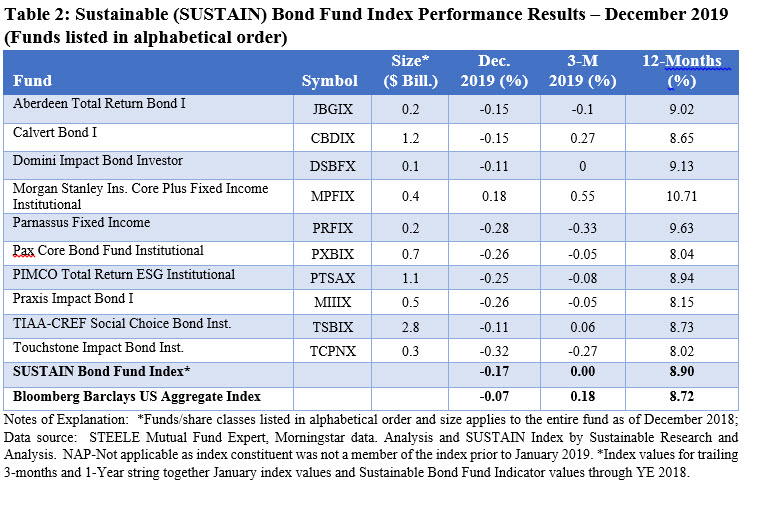

Investment-grade intermediate funds posted a negative return for the second consecutive month as did the SUSTAIN Fixed Income Fund Index. Further, the SUSTAIN Index lagged the Bloomberg Barclays US Aggregate Index (BB) again this month, posting a return of -0.17% versus the conventional benchmark’s -0.07% while investment-grade intermediate funds posted a negative return for the second consecutive month. Only one of ten SUSTAIN index members posted a positive result while the other nine failed to match or beat the BB Index. The exception was the Morgan Stanley Institutional Core Plus Fixed Fund I that gained 0.18% in December, likely benefiting, in part, from its lower BB average credit quality positioning as well as 8.75% cash position. The fund also led in the 4th quarter and 2019 calendar year with a long-term average equity like return of 10.71%. Refer to Table 2.

Laggards included Touchstone Impact Bond Institutional, -0.32%, Parnassus Fixed Income, -0.28% and Pax Core Bond Institutional as well as Praxis Impact Bond I, both of which recorded -0.26% returns.

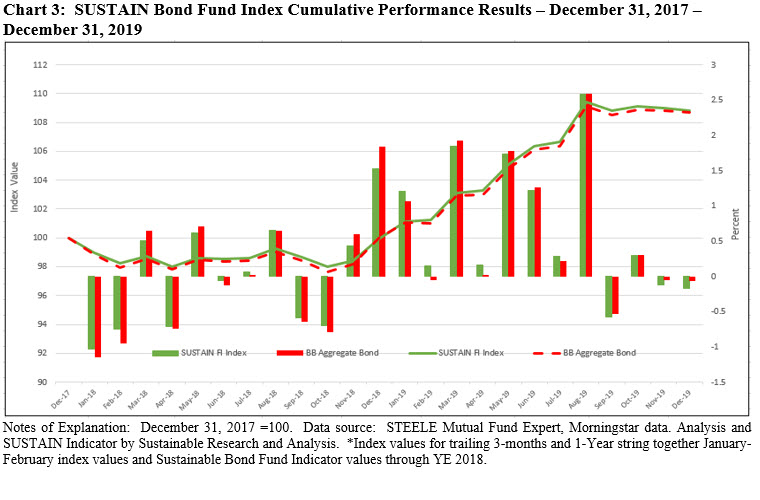

The SUSTAIN Fixed Income Fund Index has now lagged the conventional index for the fifth consecutive month. While it underperformed during the last quarter, on a year-to-date basis the index leads by 18 bps as seven of the index members exceeded the performance of the Bloomberg Barclays US Aggregate Index. For the year, the SUSTAIN Index is up 8.90% versus 8.72% for the Bloomberg Barclays US Aggregate Index and since its inception as of December 31, 2017, the return delivered by the Index is 8.8% versus 8.73% achieved by the conventional benchmark, for a differential of 0.07 bps. Refer to Chart 3.

Sustainable (SUSTAIN) Foreign Equity Fund Index strong gain of 3.53% not sufficient to beat the conventional index

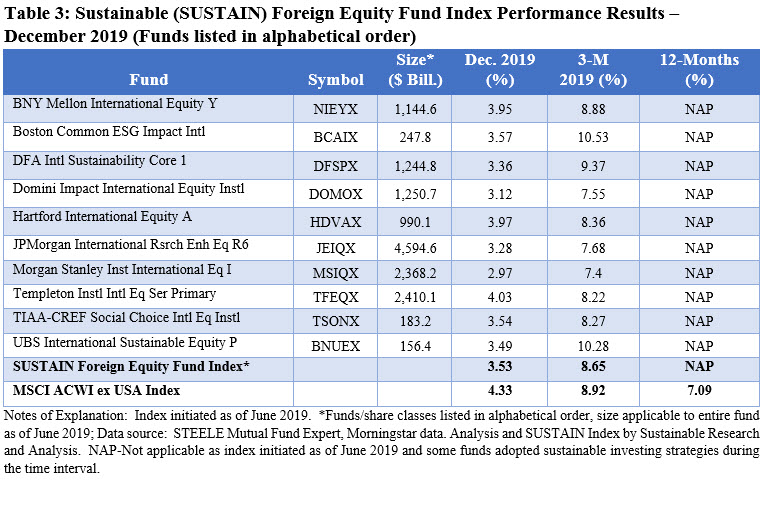

After a four-month winning streak, the SUSTAIN Index reversed course and fell behind the MSCI ACWI ex USA to closed the month of December at 3.53%. The SUSTAIN Index outperformed its domestic US counterpart but lagged its conventional index by 61bps as none of the component funds beat the conventional MSCI index. The one fund to come closest with a return of 4.03% is the Franklin Institutional International Equity Series Fund Primary Shares. This large-cap value oriented fund that integrates ESG benefited from its value orientation during a month when value outperformed growth stocks by 4 basis points. The fund’s 43% overweight position in developed European markets also likely contributed to performance as Europe eclipsed other developed markets in Asia and Latin America. At 3.95%, the second best performing SUSTAIN Index fund member, the BNY Mellon International Equity, also benefited from its developed European markets overweight position at 43.56% and, in particular, UK allocation of 22.95%. The fund’s allocation to the Healthcare sector, with top names such as Novartis AG, Roche Holding and GlaxoSmithline PLC that make up three of the fund’s top five names were additive in December. The $271.2 million Boston Common ESG Impact International Fund came in third, and also delivered the second best performance in 2019 with its 23.74% return, behind DFA International Sustainability Core 1 Fund that added 24.21% in 2019 versus 21.51% for the conventional index. Refer to Table 3.

Laggards for the month included Morgan Stanley Institutional International, Domini Impact International Equities and JPMorgan International Research Enhanced Equity R6 with returns of 2.97%, 3.12% and 3.28%, respectively.

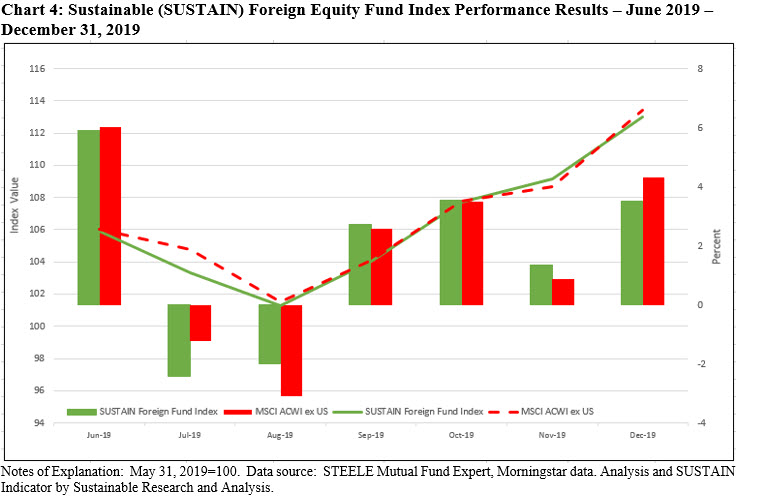

Beyond the month of December, the SUSTAIN Foreign Equity Fund Index since its inception as of 6/31/2008 lags slightly with a return of 13.03% versus 13.4% for the conventional MSCI ACWI Index, ex USA. Refer to Chart 4.

Sustainable Indices Lag in December but Excel in 2019

Stock and bond markets worldwide posted excellent returns in 2019 bolstered by strong December gains: S&P 500 added 3.0% while the Dow Jones Industrial Average and Nasdaq Composite recorded 1.9% and 3.6% increases. Stock and bond markets worldwide posted excellent returns in 2019. The major US stock indices ended the last day of the year…

Share This Article:

Stock and bond markets worldwide posted excellent returns in 2019 bolstered by strong December gains: S&P 500 added 3.0% while the Dow Jones Industrial Average and Nasdaq Composite recorded 1.9% and 3.6% increases.

Stock and bond markets worldwide posted excellent returns in 2019. The major US stock indices ended the last day of the year on a positive note, bolstered by encouraging news that the US China Phase 1 trade agreement will be signed on January 15 and signaling a significant de-escalation of trade tensions between the two nations that have affected markets throughout the year both positively and negatively. This factor, combined with interest rate cuts, Fed liquidity, easing anxiety regarding the strength of the US economy and prospects that the longest expansion in US history will continue, moved markets higher in December notwithstanding lingering geopolitical as well as domestic political uncertainties linked to the President’s impeachment proceedings. The S&P 500 posted a total return gain of 3.0%, while the Dow Jones Industrial Average and Nasdaq Composite recorded 1.9% and 3.6% increases. Outside the US, developed and emerging market equities posted even stronger returns, with the MSCI ACWI ex USA (Net) gaining 4.3% and emerging markets climbing 7.5%. Across other asset classes, investment-grade bonds continued to decelerate and dropped -0.1% while gold and energy, in that order, recorded increases of 3.6% and 6.9%. Within the Energy sector, natural gas was the only commodity to fall back, giving up -3.0%.

Against this back-drop, sustainable mutual funds and ETFs across all categories combined posted an average 2.29% total return. More targeted, the Sustainable (SUSTAIN) Large Cap Equity Fund Index gained 2.92% while the SUSTAIN Foreign Equity Fund Index and SUSTAIN Bond Fund Index generated total returns of 3.53% and -0.17%, respectively.

Starting the month of December in the red, the S&P 500 Index hovered in negative territory until December 11 when it kicked up and registered successive but small, less than 1%, gains thereafter. Refer to Chart 1. The market was encouraged by vows on the part of the European Central Bank as well as the US Federal Reserve to support their respective economies. In the US, the Fed’s remarks were made following its decision to keep interest rates on hold. Also during that same week, the Conservative Party led by Boris Johnson won the United Kingdom’s election and in the US the announced US–China Phase 1 mini deal halted the December 15 tariff increases. At the same time, investors were not deterred as the House Judiciary Committee approving two articles of impeachment against President Trump. These developments, reinforced by a string of positive economic news, sustained positive investor sentiment for the remainder of the month of December that led to a series of new market setting records. The Dow Jones Industrial Average and S&P 500 posted new record highs on December 27th and the Nasdaq Composite did so on December 26th. This put the stock market in the US at very high trading levels that, by some measures, such as the Cyclically Adjusted Price Earnings (CAPE) ratio, signaled a note of caution. The ratio now stands at 31, reflecting a level observed only twice before—in 1929 before the stock market crash and in 1999 just before the internet bubble drop. Yet, earnings have stagnated recently and earnings estimates for calendar year 2020, even as they are ascribed an above average earnings growth rate of 9.6% at this time, are likely to ratchet down.

The U.S. economy is entering 2020 along a path that many believe supports the continuation of the longest economic expansion in US history. Real gross domestic product (GDP) increased 2.1% in the third quarter of 2019, according to the “third” estimate released by the Bureau of Economic Analysis in late December. The growth rate was unrevised from the “second” estimate released in November. In the second quarter, real GDP rose 2.0%. Moreover, consumer spending which accounts for almost two-thirds of U.S. economic activity was showing signs of improvement. Per the Commerce Department, consumer outlays increased 0.4% in November, its strongest gain since July. The labor market is tight, the unemployment rate is at a 50-year low and real disposal personal income also increased at a 2.9% annual rate in the third quarter. Unless derailed by geopolitical and domestic political developments, these and other positive indicators suggest that the economy will keep expanding but, based on economic projections, at a slower rate. For example, Morgan Stanley’s base-case outlook calls for U.S. GDP growth of 1.8% in 2020.

The 4th quarter: S&P 500 added 9.1%, DJIA increased by 6.7% and Nasdaq Composite gained 12.5%

Benefiting from successive monthly gains, stocks markets in the US and overseas posted strong growth rates in the fourth quarter. The S&P 500 added 9.1%, the DJIA increased by 6.7% and the Nasdaq Composite charged ahead with a gain of 12.5%. 10 of eleven large-cap sectors also recorded increases, with Information Technology and Healthcare both adding 14.4%. Real Estate, on the other hand, gave up -0.5%. Developed and emerging markets in Europe, Far East, Asia and Latin America also recorded strong gains ranging from a low of 7.1% for the Pacific Region to a high of 14.8% delivered by Eastern Europe, as measured by the MSCI regional international indices. Local markets such as Taiwan, Russia and China posted gains of 18.0%, 17.1% and 14.7%, respectively. The SUSTAIN Indices followed suit, but in each case lagged behind their conventional indices by as little as 18 bps and as much as 66 bps.

The year 2019: S&P roars back with a gain of 31.5%; bonds gain 8.7%

The year in stocks and bonds experienced an unexpected reversal after large cap stocks tumbled some 15% between the end of November and December 24, 2018 on US-China trade uncertainties, recession fears and tightening monetary policy. After ending the year down -4.4%, the S&P came roaring back in 2019 to post a gain of gain of 31.49%, the best gain since 2013 and 25.4% points above the 6.1% average for the last 20 years. The DJIA gained 25.3% and the Nasdaq Composite lead with a gain of 36.7%. Stocks and bonds benefited from falling interest rates, Fed liquidity, receding trade tensions and rosier expectations for economic growth. Growth stocks across the small and mid-cap market spectrums outperformed value stocks while large cap growth and value stocks performed on par. Very large growth stocks (i.e. top 200) outperformed very large value stocks while large caps were just about even. At the same time, small cap stocks fell behind their large cap counterparts by as much as 8.3%, depending on the benchmark.

As for bonds, the Bloomberg Barclays US Aggregate Index added a whopping 8.7% in 2019, the best annual results in the last ten years and 3.7% higher than the 20-year average. Even better 2019 results were posted by long-dated US Treasuries, up 15.1% while US credit added 13.8% as the environment throughout the year remained supportive.

Markets outside the US didn’t reach the highs achieved in the US. The MSCI ACWI, ex USA (Net) was up 21.51%, Europe and emerging market composite came in even lower while a number of national indexes, such as Russia and Taiwan, in particular, gained 52.7% and 37.7%, in that order.

Sustainable (SUSTAIN) Large Cap Equity Fund Index misses S&P 500 by 10 bps

Off by 10 basis points, the SUSTAIN Large Cap Fund Index lagged the S&P 500 for the fourth consecutive month as only four of the ten fund constituents underperformed in December. The Pax Large Cap Fund Institutional Shares led with a 3.46% return, bolstered by the $766.3 million fund’s overweight exposure to the technology sector that gained 4.5% in December as well as stock selection. In particular, above index exposure across its top five holdings, including Apple, Microsoft, Amazon, P&G which was added in the first part of the year and was viewed as an ESG leader, and Merck & Co., all performed well in December. Returns for these five stocks ranged from 2.5% to a high of 9.9% posted by Apple which accounted for 5.62% of the fund’s holdings. At the same time, the fund’s reduction in its energy position to 0.0% ahead of December when energy was up 6.0%, likely detracted from its performance. Two other performance leaders include JPMorgan US Equity R6 and TIAA-CREF Social Choice Equity Fund Institutional Shares that added 3.37% and 3.34% in December. While ranked second in December, the JPMorgan fund was the best performer over the previous two months and has delivered an above benchmark return of 10.46% in the fourth quarter. Refer to Table 1.

At the other end of the range was Parnassus Core Equity Investor. The fund, which seeks low turnover and invests with a high conviction in approximately 40 holdings while avoiding investments in companies engaged in the extraction, exploration, production or refining of fossil fuels, trailed the S&P 500 by 98 bps in December and 281 bps in the last quarter. The fund’s overweighting in industrials while at the same time avoiding the energy sector likely detracted from its performance. Other lagging funds included Calvert Equity A which fell behind with a 2.2% return while still retaining its top performer status for 2019 and Pioneer A that generated a 2.64% return and now also lags behind the S&P 500 for the quarter and 12-month interval.

Over 2019, the SUSTAIN Large Cap Equity Fund Index outperformed the S&P 500 but since inception as of December 31, 2016, the Index is up 49.2% versus 53.1% for the S&P 500. Refer to Chart 2.

Sustainable (SUSTAIN) Fixed Income Fund Index lags for the second consecutive month

Investment-grade intermediate funds posted a negative return for the second consecutive month as did the SUSTAIN Fixed Income Fund Index. Further, the SUSTAIN Index lagged the Bloomberg Barclays US Aggregate Index (BB) again this month, posting a return of -0.17% versus the conventional benchmark’s -0.07% while investment-grade intermediate funds posted a negative return for the second consecutive month. Only one of ten SUSTAIN index members posted a positive result while the other nine failed to match or beat the BB Index. The exception was the Morgan Stanley Institutional Core Plus Fixed Fund I that gained 0.18% in December, likely benefiting, in part, from its lower BB average credit quality positioning as well as 8.75% cash position. The fund also led in the 4th quarter and 2019 calendar year with a long-term average equity like return of 10.71%. Refer to Table 2.

Laggards included Touchstone Impact Bond Institutional, -0.32%, Parnassus Fixed Income, -0.28% and Pax Core Bond Institutional as well as Praxis Impact Bond I, both of which recorded -0.26% returns.

The SUSTAIN Fixed Income Fund Index has now lagged the conventional index for the fifth consecutive month. While it underperformed during the last quarter, on a year-to-date basis the index leads by 18 bps as seven of the index members exceeded the performance of the Bloomberg Barclays US Aggregate Index. For the year, the SUSTAIN Index is up 8.90% versus 8.72% for the Bloomberg Barclays US Aggregate Index and since its inception as of December 31, 2017, the return delivered by the Index is 8.8% versus 8.73% achieved by the conventional benchmark, for a differential of 0.07 bps. Refer to Chart 3.

Sustainable (SUSTAIN) Foreign Equity Fund Index strong gain of 3.53% not sufficient to beat the conventional index

After a four-month winning streak, the SUSTAIN Index reversed course and fell behind the MSCI ACWI ex USA to closed the month of December at 3.53%. The SUSTAIN Index outperformed its domestic US counterpart but lagged its conventional index by 61bps as none of the component funds beat the conventional MSCI index. The one fund to come closest with a return of 4.03% is the Franklin Institutional International Equity Series Fund Primary Shares. This large-cap value oriented fund that integrates ESG benefited from its value orientation during a month when value outperformed growth stocks by 4 basis points. The fund’s 43% overweight position in developed European markets also likely contributed to performance as Europe eclipsed other developed markets in Asia and Latin America. At 3.95%, the second best performing SUSTAIN Index fund member, the BNY Mellon International Equity, also benefited from its developed European markets overweight position at 43.56% and, in particular, UK allocation of 22.95%. The fund’s allocation to the Healthcare sector, with top names such as Novartis AG, Roche Holding and GlaxoSmithline PLC that make up three of the fund’s top five names were additive in December. The $271.2 million Boston Common ESG Impact International Fund came in third, and also delivered the second best performance in 2019 with its 23.74% return, behind DFA International Sustainability Core 1 Fund that added 24.21% in 2019 versus 21.51% for the conventional index. Refer to Table 3.

Laggards for the month included Morgan Stanley Institutional International, Domini Impact International Equities and JPMorgan International Research Enhanced Equity R6 with returns of 2.97%, 3.12% and 3.28%, respectively.

Beyond the month of December, the SUSTAIN Foreign Equity Fund Index since its inception as of 6/31/2008 lags slightly with a return of 13.03% versus 13.4% for the conventional MSCI ACWI Index, ex USA. Refer to Chart 4.

Premium Articles Access Priority Support 1 Fixed Price

Access to All Data No Credit Card Required Cancel Any Time

Access to Premium Articles Priority Support Save 25%

$99

PER YEAR

Access to exclusive content

Premium Articles

Access 1 Fixed Price

Free Trial

30-Day

Access to exclusive content

Access to All Data No Credit card Required Cancel Any Time

$9.99

MONTHLY

Access to premium content

Access to premium Articles Save 25%

Sustainable Funds Monitor

Funds Glossary

Quarterly On-Line Briefings

Sign up to free newsletters.

By submitting this form, you are consenting to receive marketing emails from: . You can revoke your consent to receive emails at any time by using the SafeUnsubscribe® link, found at the bottom of every email. Emails are serviced by Constant Contact